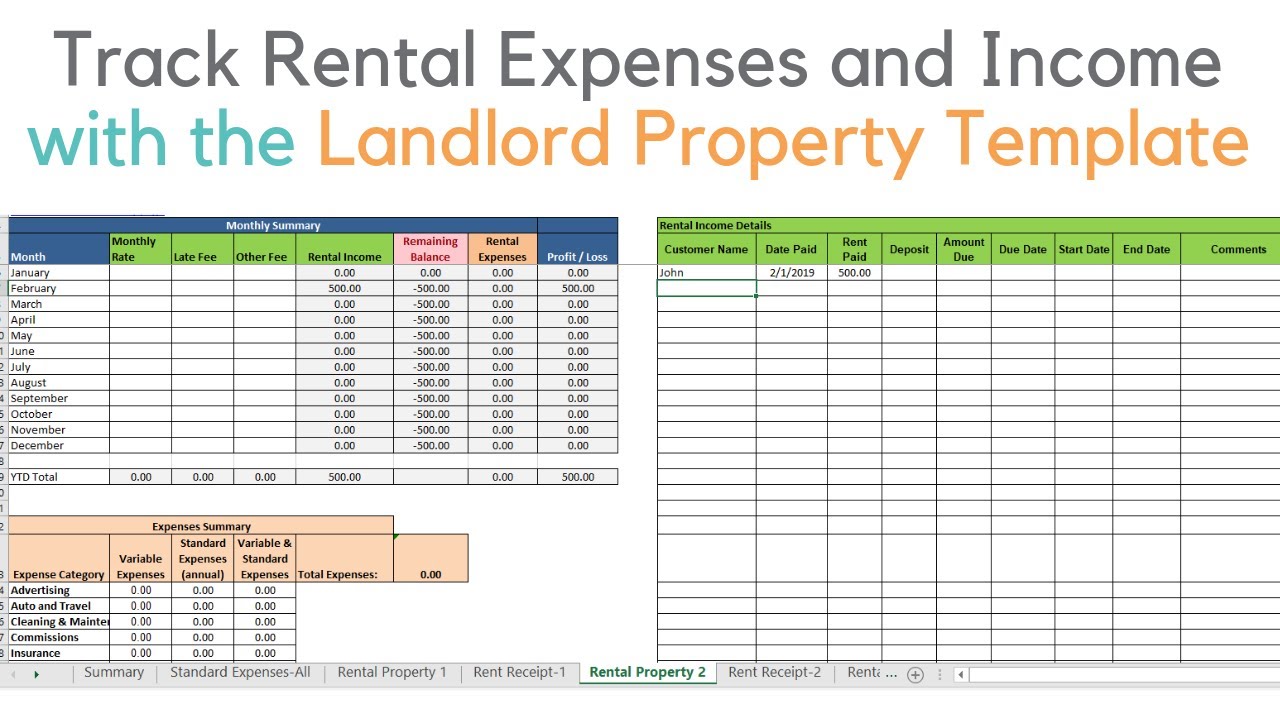

Simplifying Profit and Loss Calculations for Landlords

Hire houses can be considered a lucrative organization, but the economic part involves cautious administration, particularly when it comes to gain and loss reports. These studies are a key instrument to evaluate your rental money, expenses, and overall profitability. However, actually skilled landlords often make errors that can result in financial setbacks or incorrect ideas within their rental property spreadsheet performance. Here is a review of some common problems to avoid.

1. Underestimating Maintenance Fees

Many hire property owners forget to account for continuing preservation within their gain and loss reports. Fixes and routine preservation, such as for example HVAC maintenance, pest get a grip on, or plumbing fixes, are regular expenses. Failing to allocate funds for such expenses can build an inaccurate representation of one's profitability. Authorities frequently suggest setting aside 1% of the property's annual price for preservation costs.

2. Ignoring Vacancy Intervals

Vacancies are inevitable but frequently ignored in gain and reduction calculations. Whether it is a tenant turnover time or market downturn, these holes mean zero rental revenue while costs like mortgage payments, resources, or house fees stay constant. Including an estimated vacancy rate in your confirming provides an even more practical financial outlook.

3. Misclassification of Costs

Exact categorization of costs is crucial. Mixing particular costs with property-related charges on the record is a frequent error landlords make. For example, bunch energy costs for personal house along with rental home utilities distorts price tracking and complicates tax deductions. Sustaining split up reports for business-related transactions is a good practice.

4. Forgetting Depreciation

Depreciation is a significant part of home control, and overlooking it can result in underreporting expenses. Many landlords overlook to calculate depreciation on the house itself or its furnishings and appliances. This really is not only essential for knowledge your long-term expenses but also essential for leveraging tax benefits.

5. Overlooking Smaller Expenses

It's popular to skip smaller expenses like marketing fees, turnover washing, or home inspections. These small expenses can accumulate over time, skewing your perception of net income. Maintaining step by step records of all expenses guarantees precision and shows a complete photograph of one's financial health.

6. Not Frequently Updating Studies

Failing to regularly update gain and reduction studies is still another important pitfall. Property markets, hire money, and expenses change frequently. Periodic revisions not only give a definite understanding of recent economic rankings but also prepare you for tax conditions and aid in pinpointing trends.

By avoiding these popular problems, you may ensure your hire house gain and reduction reports are precise, trusted, and a true reflection of how well your expense is performing. Going for a aggressive approach to financial administration not only helps in decision-making but also sets the basis for long-term success. Always double-check your entries, and when in uncertainty, consult with a specialist to increase the possible of your investment.